TikTok is an undeniably influential social media platform with significant untapped potential for sponsored content. Following the pandemic, our habit of using TikTok remained strong. The app enjoys one of the highest user retention rates globally. An incredible 81% of users say TikTok videos influenced their recent purchases. That is why it is becoming increasingly important for brands to understand how to create effective ads that resonate with their consumers.

According to our most recent two-wave global study, we discovered that 71% of TikTok users stop and watch the first three seconds of the video and that 56% of each sponsored content is seen on average. All of this is supported by the fact that the ads are liked by 73% of TikTok users.

These figures show that sponsored content has every reason to thrive in TikTok’s digital environment. However, brands are still not using their full potential. This study not only invites you to use TikTok to empower your brand, but it also gets deep into what you must keep in mind while doing so. If you are interested in getting an expert walkthrough of the study, write us at [email protected]

Methodology

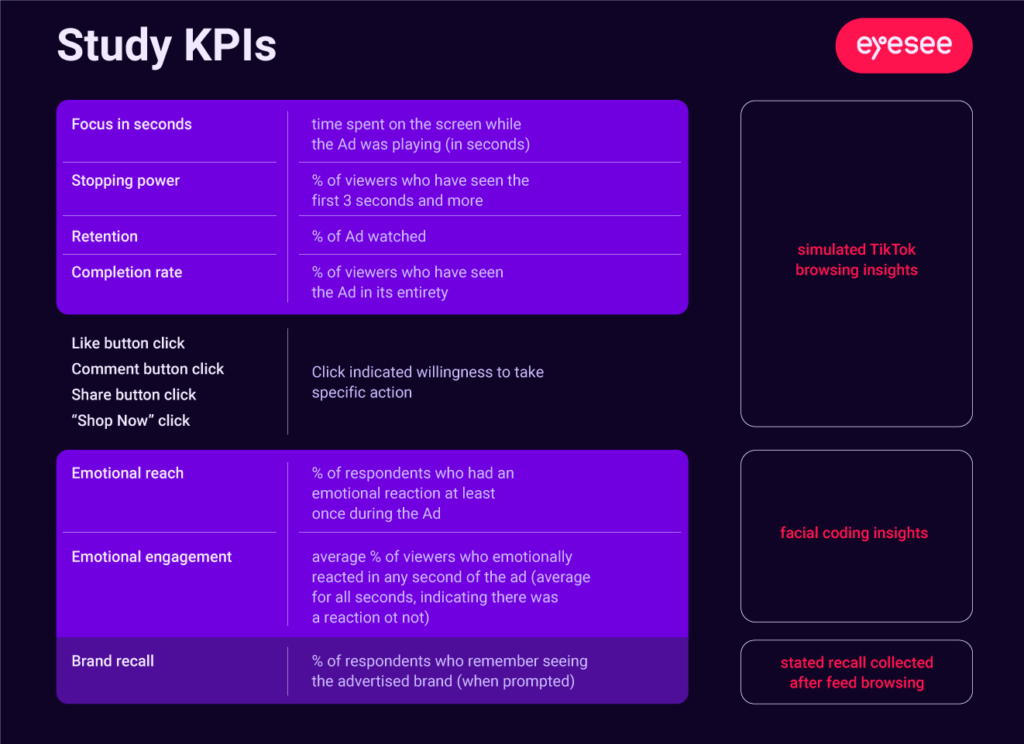

As previously stated, we tested 60 ads from 20 brands across markets and industries such as FMCG (Fast Moving Consumer Goods), Beauty, Insurance, Fashion, Technology, Automotive, Retail, etc. TikTok simulations, standalone ads, and surveys were tested among 7280 respondents.

This research is built on the following key pillars:

Ad stopping power (tested the ads in a simulated TikTok environment that provided us with browsing insights)

Ad retention (tasted by exposing respondents to a simulated TikTok environment)

Ad emotional reach (tasted by exposing respondents to standalone ads and utilizing face coding methodology)

Ad likability (tasted by exposing respondents to standalone ads and utilizing face coding methodology)

Brand recalling (to learn % of respondents who remember seeing the advertised brand when prompted, we used the survey method)

The challenge of TikTok advertising

Why don’t brands use TikTok more? This is the imposing question that arises when we look at the numbers that show the untapped potential. On one hand, we have the answer that for brand managers, it is hard to follow the ROI once they invest in TikTok ads. They are unsure how to follow the path and make a clear connection, or better to say, they are unsure how to follow the path to purchase from the TikTok ad to the shopping cart.

On the other hand, even when clarity in that field is gained, the questions of how to approach strategy and what works best remain. There are questions about what will work better – the native approach or strongly branded videos that will also work on other platforms; what is the reach of animation as the dominant style; and is co-branding the way to more followers and engagement or the way to poor brand recollection?

This study answers all those questions and beyond. For example, animated video ads, those containing any kind of computer-generated imagery, will improve brand opinion by 23% and increase brand interest by 19%, while elevating the positive emotions about the brand by 20%.

However, brands must be careful; there is a chance that they will be seen as less informative than conventional videos if the message and narrative in them are not constructed carefully.

The golden rule for unlocking the untapped potential

What is great about this report is that it contains a lot of simple facts that must be considered in future ad planning. For example:

If the ad lasts up to 10 seconds, it has a 71% higher chance of being fully viewed.

A video that lasts up to 10 seconds has a 38% higher chance of being liked.

If the brand lasts up to 10 seconds, it has a 15% better chance of being remembered.

This is an example of an insight finding that makes a strong recommendation that is universal around the world. However, in this report, there are far more complex recommendations that necessitate a thorough examination of both specific brand values and the TikTok environment.

All of this is only the beginning. If you want to learn more, send an email to [email protected] and we will provide you with a video expert walkthrough of the study. Not only will you get the big picture and the future framework for making strategic TikTok ad planning decisions, but you will also be able to formulate specific questions for your specific pain points, which we will gladly assist you with.

Request access to

TikTok creative study findings!

Eager for more? Read the blog about replicated feeds for authentic behavior here.

For two decades, Greenbook’s GRIT Reports have been the go-to resource for tracking trends in the insights industry, empowering brands, suppliers, and professionals to succeed. The annual Insights Practice Report focuses on essential approaches and skills, providing a comprehensive guide for growth.

EyeSee debuted on the GRIT Top 50 most innovative research suppliers list this year,among fourteen other tech-enabled companies. Tech-driven suppliers are rapidly gaining market and mind share; the industry is on a continued search for solutions outside of the “usual suspects” and “challenger brands” that provide alternative research frameworks.

The CEO of EyeSee, Joris De Bruyne, who has witnessed firsthand the team and client list growth over the past few years, offered the following observation:

‘Businesses like EyeSee, which focus on applied behavioral testing, make a big contribution to what the market research industry views as innovative. We are constantly finding new ways to combine methods, scale them via technology, and uncover true reasons behind consumer decisions. High predictive power of behavioral insights is the main driving force of our innovative initiatives and reason why more than one half of top 30% CPG brands place their trust in us when in need of research.”

Joris went on to explain that the EyeSee team is proud to be listed in the GRIT report with so many well-known figures who consistently motivate EyeSee to do even better. Novak Marinkovic, the Head of Research and Development at EyeSee, provided the following perspective on what is to come:

‘The report data demonstrates that technological investment increased as the pandemic spread and has continued to be significantly higher than pre-pandemic scores. EyeSee has always given applied technology a high priority; it is in our DNA. Over the years, we’ve introduced technologies to improve the output’s speed and accuracy. Currently, our primary focus encompasses two vital topics: (1) the development of social media replicas and the Collab platform, and (2) continual development of social media replicas as testing environments in order to meet ever-evolving trends and demands of our clients.’

The GRIT Top 50 list signals our industry’s direction: increased supplier diversity, tech-led growth, and an emphasis on real innovation. To access the full annual Insights Practice Report and Top 50 most innovative research suppliers list, request access here

We learned a lot about the shift in consumer behavior after the pandemic and during inflation from a recent meta-analysis study conducted by EyeSee. However, different perspectives shed light on different challenges and opportunities. EyeSee excels in connecting and scaling global knowledge since it operates in 50+ territories, constantly accumulating insights through deep behavioral analysis in a wide range of industries.

Our data, insights and business experts, all of whom came from different places, told us how they see consumer behavior changing, what kind of innovation they hope for, and what their predictions for 2024 are.

Perspective #1: APAC aims that traditional beauty ingredients become global trend

We’re a diverse market with varying external influences that shape our choices.

The rising costs of living and inflationary pressures are global phenomena that we’re also exposed to.

Yet, the recent COVID crisis has also brought the need for self-care practices to the fore—one that encompasses emotional, mental, and physiological care.

As a self-care advocate and a researcher working a lot in the beauty industry, what makes me excited is to see how brands can connect these phenomena to offer us affordable luxuries in the beauty and personal care space.

Particular to Asia is also our usage of traditional skincare ingredients that vary across the different cultures here. This offers a rich playing field for brands to provide beauty seekers here with a modern take on natural, wellness-inspired beauty products. For instance, Bakuchiol (used in traditional ayurvedic treatments) arose as an alternative to the popular retinol.

In 2024 and the years to come, I would love to see how ingredients used in traditional Asian skincare treatments would be recognized and amass greater mainstream popularity.

Perspective #2: LATAM is all about brand-alliances and cross-selling

I think brand loyalty is being tested since incomes at home are not enough due to the crisis; people might be switching to cheaper brands or avoiding certain expenses while at the same time spending money on entertainment because of COVID-19 post-lockdown. In markets where the economy is more unstable, things are getting much harder.

There are new flavors in the FMCG category (biscuits, chips, sodas), including brand alliances and the usage of brand licenses for cross-selling, but as a movie fan, the ones I have my eyes on are the new popcorn flavors in cinemas.

It’s hard to pick one future trend because there are a lot of trends lately: eco-friendly products, light/zero sugar versions of some things, but I think consumer experience will become more relevant, so I think we will see a lot of “memory makers” (people making up for the “lost” time and trying to document every moment) reconnecting with things, trying to be heard and seen.

Perspective #3: Sustainability is still strong trend in EUROPE

Given this is a global crisis, we in Europe are also strongly affected by the effects of soaring inflation, and with mortgage payments starting to go up for many, shoppers’ disposable income is being squeezed.

In the UK specifically, food has seen some of the highest levels of inflation and considering 86% of people are looking to improve their health, it’s a struggle to do so when these items are usually more expensive.

I think the biggest area of innovation will continue to be sustainability, and I’ve seen some great recent examples, like Penny in Germany launching a ‘true cost’ campaign to raise awareness of the environmental price of producing food; or rolling out our digital screens and labels to reduce waste in stores.

Sustainability, as we saw with Penny, will continue to be important for consumers, and therefore innovation is needed here.

I’m very excited to see what role AI will play in CPG next year! I recently saw that Migros launched the world’s first AI-created drink, where ChatGPT generated the recipe based on recent trends, and the packaging was created by another AI tool called Midjourney. Where next?

Perspective #4: USA consumer confidence and optimism is coming back

Despite a difficult economic climate right now in the US which continues to be shrouded in uncertainty, consumer confidence and optimism is slowly improving relative to where it was just a year ago. Consumer spending remains strong, however, they are more cautious about how and where they spend their money. A spending paradox has emerged… On one hand, consumers are making more choiceful purchase decisions – in some cases seeking greater value by trading down to less expensive store-brand items to maximize their spending power. Despite this, there is a clear openness to splurge – to treat oneself by paying premium prices for higher-quality products or those that are driven by spontaneous cravings.

I am excited to see the unique products that emerge following the sale and acquisition of several CPG firms that took place in 2023 and the strong desire by key companies to create news within their respective categories (blending brands, blending product benefits, and core product equities into new products). Companies are constantly looking to expand their offerings to attract new customers, and I think the competition in the industry right now may help to inspire new innovative creativity that will drive unique products to market.

I think, we are going to see a major boom in social commerce spending – particularly on TikTok. Social media has emerged as a powerful platform for driving product discovery and promoting ecommerce. In 2023 we saw brands registering success with TikTok ad campaigns and I suspect that in 2024 we will see a major surge as many others follow suit. With so many younger consumers using TikTok to discover, research, and offer their impressions on products, I foresee that TikTok will naturally become a more relevant part of their shopping process.

Every territory and every market has its own rules, but maybe it is exactly in the differences between the untapped opportunities lie. It is not uncommon for local trends to become global and vice versa, so keeping your eyes on all four sides of the world is strongly recommended.

Interested in diving deeper into consumer behavior knowledge, tune in and follow our podcast you can acquire here.

Like people, no brand is an island that exists apart from its context. Especially if the product is dominantly distributed through retail systems. Retail systems are like a whole different planet, and categories are like different parts of that world, each with “their own culture”.

However, considering the category is not just about gaining a much-needed understanding of the context; it is also about untapped growth potential and potentially missed opportunities. Not only that, but how can a brand be relevant if it does not follow the trends of its own category unless its mission is to be disruptive and deliberately goes against them?

What is a category growth strategy?

Oksana Sobol, Insights Lead at Clorox Company, said in Deep Dive episode six, “Why context is king for category leadership,” that a business planning process might undergo change where it starts with a vision for a category rather than a brand.

She pointed out that there are several key questions that must be addressed.

What are brand hypotheses for how the entire category will grow?

How will the category evolve?

What challenges and opportunities will those hypotheses need to solve?

She then added that a mindset shift is neither enough, nor achievable without a mechanism.

“This is where concrete changes have to be made to mechanisms like the business planning process, the way we interact with our retail partners, and, critically, the way the Insights team supports this approach.”

In researcher terms, it means testing everything you can (pack design, displays, NPDs) in context, in a real environment. However, for tasting to be fast, “real environments”, are usually virtual environments – which have a striking 0.9 correlation with offline shopping, so they are scalable and definitely more affordable. Going beyond pack, display, and planogram testing, it is the most critical for context understanding to add behavioral Decision Tree studies, which tell us how people make decisions within the entire category and the importance and hierarchy of decisions. When we use Decision Tree studies, we are not only knowledgeable of the role that every product in a category has but also of the role of every product within one brand’s portfolio.

The benefits of a category growth strategy

As mentioned in previous article about brand blocking, it is all about finding a way to get that ‘triple win’ we all strive for and tactics that benefit:

the consumer

your brand

and the total category

Once that is achieved, the benefits are easy to see. First and foremost, there is a satisfied consumer since you can always foresee how their needs are changing, and, therefore, how the category’s offering needs to change to ensure it remains relevant and continues to recruit new shoppers on new occasions.

Second, if the point of purchase is improved by creating a simple, intuitive, but engaging place to shop that cut through autopilot shopping and drives interest and category reassessment, as mentioned in the brand blocking article, everyone is once again satisfied. Brands are seen, purchases are made, and customers have a better shopping experience.

Third, is there anything better than having a clearly aligned pathway to growth where all sides are satisfied even before embarking on that journey? It means fewer misunderstandings and detours from the final destination, which is success.

Conclusion

When considering the category growth mindset, it may appear that it will impose not only more work for the teams, but also more complex problems that require truly creative solutions. However, when all of the benefits are considered, and once that category and brand growth are aligned, the risk that something could have a negative impact on ROI is much lower. All of those extra miles that should be walked will be those that you will not have to take in the future when time is not on your side.

Interested in category management? Check out our Deep Dive podcast episode with the Clorox Company Insights Lead.

by Mirna Djuric, Product Capability Director at EyeSee

The world has gone through quite a few disruptions over the last three years. According to CPS GfK over 60% of European households are in or close to a serious budget squeeze, with Western European countries, especially on the rise. Nearly 2 in 3 consumers declare to cut their out-of-home (OOH) spending, including visiting restaurants and bars, buying clothes (-48%), as well as gifts, decorations, and takeout/delivery (all at -46%).

But even though shoppers are more focused on preparing meals at home, the EyeSee meta-analysis shows that the food part of FMCG has suffered the most. This meta-analysis is based on 250 studies in the FMCG category. Samples ranged from 50.000 to 150.000 respondents per method, spread over 4 geographies – US, Europe, APAC, and Latin America. They included methodologies such as Eye Tracking, Facial Coding, Virtual Shopping, and surveys, and they were all done in highly realistic shelf environments that, 95% of the time, matches actual shopping behavior.

After gathering all the data, it was grouped into pre-pandemic (2018 and 2019) and post-pandemic and all subsequent events (2020-2022), and eventually compared.

Food category products are more likable but less bought

It does not appear obvious that in times when shoppers are spending more time preparing meals, food would be the most crisis-influenced category in the FMCG category. However, if we remember that one of the key takeaways from the EyeSee pricing study was that the main goal of shoppers is to spend as little as possible, even if it means buying smaller packs of products and getting less value for their money, we may be able to gain a better understanding of this type of behavior. Food products are the ones we buy every day, and we can see their price increases getting higher and higher, whereas, in other non-food categories, we do not buy as frequently, so we do not have a sense of their impact on our overall budget.

However, when shoppers are directly asked about the products, they will react positively and describe them as highly desirable, keeping in mind that we all want to resume our pre-pandemic lives as soon as possible. But what they will buy is a different story.

In the food segment of FMCG, both consideration and penetration rates have decreased by more than double. Simply put, fewer people are buying fewer products, and competition on the shelf is fiercer.

Shoppers’ exploratory behavior has also decreased, and individual SKUs and brands appear less visible on the shelf. Shoppers appear to spend more time finding exactly the product they intend to buy and less time exploring other options.

Visibility in the first 5 seconds dropped significantly, as did attention to the key zone, meaning shoppers’ exploratory behavior decreased and they are possibly spending time on shelves analyzing price tags instead of browsing products.

However, the likability of products significantly increased, meaning they were found to be more and more attractive and relevant.

Is e-commerce a saving grace for FMCG in the US?

With increased e-commerce spending, we can expect that FMCG in the US will potentially remain healthy. It is also interesting for this market that on the pack navigation, the US stands out by brand importance.

This is the only region where brand logos are gathering more consumer views. Like other markets, secondary images lost visibility while claims gained it. This suggests shoppers want to be more certain they are getting the product they intended to buy beforehand, meaning shopping is more targeted.

Very similar patterns are evident in the European markets as well; although actual shopping hasn’t yet universally decreased, there are indications that shoppers are more cautious (relying on tried-and-true brands) and therefore less exploratory.

The nonfood category remains stable but claims gain importance

Even though non-food products are still in the same or similar demand, and even though post-pandemic cravings among shoppers are strong, when spending money in times of crisis, they may feel the need to justify their spending, so they will turn to claims and question them, having more information now than during carefree pre-pandemic times.

This higher level of caution is confirmed when looking into navigation patterns in the non-food category. Claims have gained significantly more consumer looks resulting in a 50% increase in claim visibility. Other pack elements, particularly imagery, both primary and secondary, suffered in consumer attention.

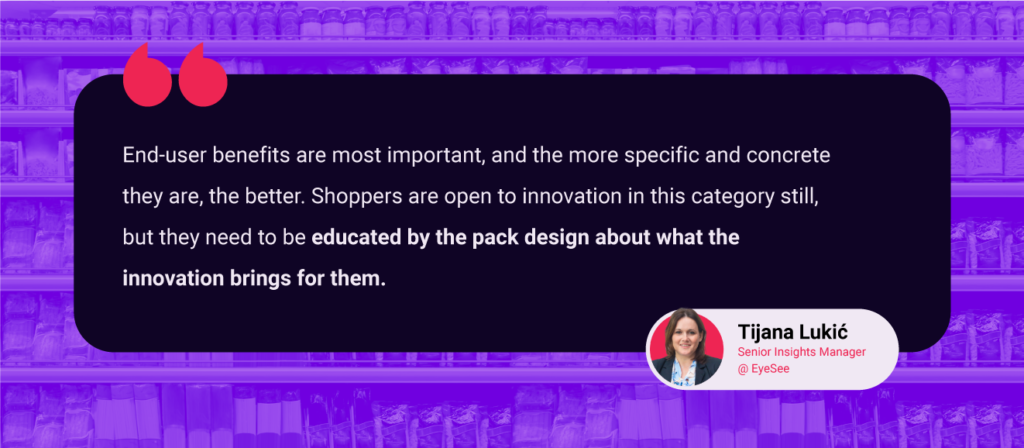

Our packaging and claim expert, Tijana Lukic, provides more context in terms of what post-pandemic consumers look for in the non-food category.

“End-user benefits are most important, and the more specific and concrete they are, the better.“ She also notices that shoppers have become true experts, they are knowledgeable about ingredients, their benefits, and their risks, so they choose cautiously.

“Shoppers are open to innovation in this category still, but they need to be educated by the pack design about what the innovation brings for them. So, the concrete benefits are appreciated. Sustainability of the product is important, but it hasn’t exited the nice-to-have category yet in most non-food categories.”

Latin American market can expect further decreases in FMCG

In the Latin American market, on the other hand, shelf purchases significantly decreased, but not only that; consumers are consciously saving. Even stated purchase intent, which usually lags the actual purchase, shows a decrease in this market. This suggests we can expect further decreases in FMCG in LATAM.

Conclusion

With all of these insights in mind, it is evident that different markets show different results depending on their strengths and weaknesses. However, the pressure of one crisis after another can be more or less felt everywhere. Even though the average consumer wishes to go back to his previously carefree life and spending, their budgets simply do not allow it.

From the producer’s perspective, category leaders are under more pressure than ever to sustain their market growth. If you are interested in this topic and want to learn more, register for GreenBook X EyeSee webinar on How Category Leaders Adapt to Post-Pandemic Consumer Behavior here – https://bit.ly/3Kwcs7D

Interested in findings from our pricing studies from the US and which categories have we researched? Read all about it here or you can check out the full webinar featuring Heather Graham (Director Client Service @ EyeSee), Sasa Radojevic (Sr Shopper Insight Manager @ EyeSee), and experienced retailer & Awarded 2022 Top Women in Grocery (TWiG) Raina Rusnak.

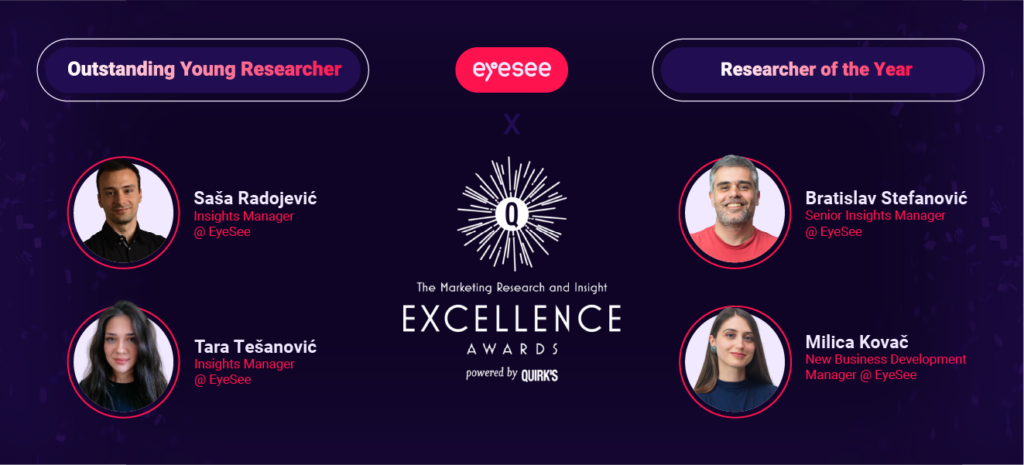

Some people hear music when they see music sheets, while others can look at the data and see valuable insights that lead to strong business development recommendations. Insight managers are a true force behind the Market Research Industry and its cornerstone, each crafting insight stories in their unique way.

We use The Marketing Research and Insights Excellent Awards powered by Quirk’s to put them in the spotlight and give them all the credit they deserve because, without them, all we would have, is a big pile of numbers and statistics we would have no idea how to use.

When did you realize you were hooked on behavioral insights and there was no going back?

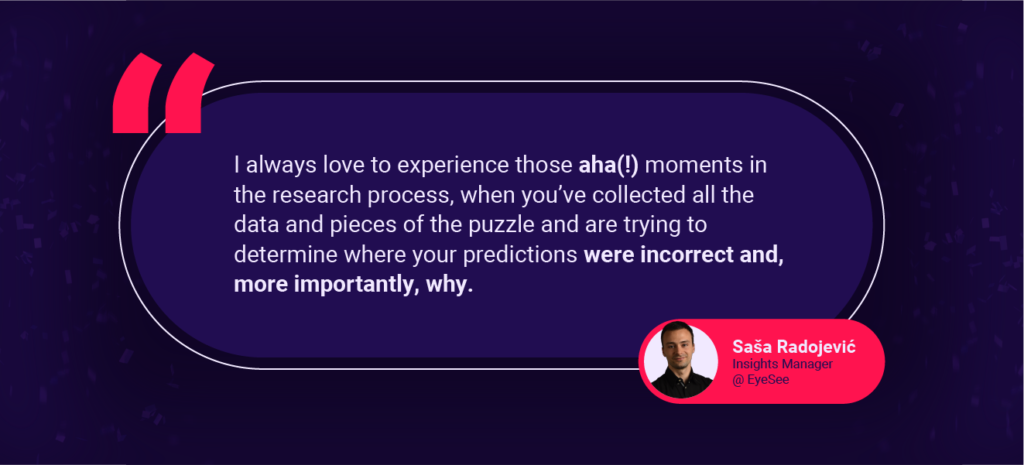

Saša: I must admit that my mentor, Beca (Dobrinka Vicentijevic), infected me with enthusiasm and passion for turning data into insights and the magic of the aha(!) moment. I always love to experience those. You collect all the data and piece the puzzle together, trying to determine where your predictions were incorrect and, more importantly, why! So, you are constantly thinking about it, trying to connect the dots. So, when thinking about it becomes an obsession, you usually let it go, take a step back, and then it just happens.

Tara: For me, it is the gap between say and do in shoppers’ behavior that is so inspiring, and I also love how the implicit approach to research effectively reveals biases. For example, the entire marketing team may be baffled as to why some packaging labels have no impact on consumers and may have a variety of design theories, but eye-tracking methodology will quickly reveal that it is because they are positioned in such a way that they are not spotted at all.

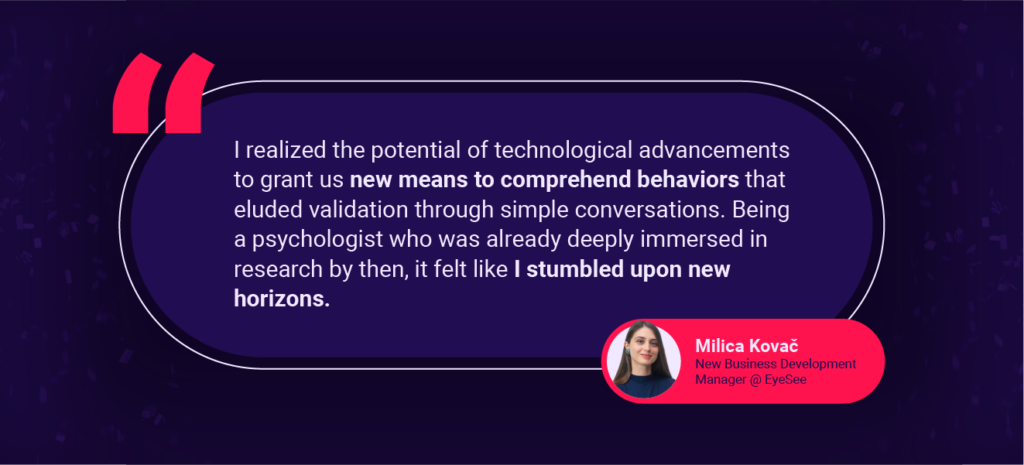

Milica: More than 5 years ago I realized the potential of technological advancements to grant us new means to comprehend behaviors that eluded validation through simple conversations. Being a psychologist who was already deeply immersed in research by then, it felt like I stumbled upon new horizons. I’m eagerly anticipating the unfolding of future technologies in our domain.

Bratislav: It was when I started realizing that it was not always easy to decipher what respondents really thought by providing their answers and opinions to our traditionally defined questionnaires. Many times, I was left with the impression that something was missing, the unfathomable part of what they really thought or needed. Over time, I learned that consumers could easily and clearly express some of their needs, and that’s where traditional questionnaires were quite useful. But oftentimes, consumers cannot articulate their needs, and their responses can then be misleading or prone to biases. This is where the behavioral approach proved to be super useful, as all I did was to just put consumers in their typical and specific situations, with little to no influence or instruction, sit back and observe, and then look for typical patterns of behavior. This way I was much more confident with the learnings and able to draw bolder conclusions and recommendations on how to influence consumers.

The last few years have been in crisis mode for most (if not all) of us. How has the consumer changed?

Saša: I understand that the expected answer should be based on our personal impressions rather than a study with specific parameters, but I am afraid that once you recognize the importance of context and put on your insights manager glasses, you cannot just assume such things. So, I will let this one slide, if that is okay.

Tara: My personal impression is that when it comes to shopping, people become much more cautious and stricter. Especially when it comes to less frequently purchased and somewhat pricey categories like care and beauty. Shoppers will question every claim made about the product, so communication must be well thought out.

Milica: Living in a deeply consumeristic society, addressing this question isn’t straightforward. If we talk about shoppers, regardless of channel, knowing that trade is a human activity that has existed for a very long time and crisis are nothing really new to people, we see how swiftly shoppers adapt their strategies when crisis hits, making more informed and conscientious choices (crises elevate the significance of System 2 decision-making); at the same time, social media and technologically mediated social communication is a relatively young phenomenon in human history and we are witnessing those same shoppers as now social media consumers struggling to consciously dispose of their time in a way that they perceive as healthy, especially during crisis.

Bratislav: We are going through the most dynamic period with dramatic changes in the behavior of all of us as consumers. The recent events, COVID pandemic, global crisis and inflation have been shaping the way we shop and consume goods and services. During the pandemic, while locked down, we turned to e-com, but limited to spend as much as wanted, given the concerns and uncertainty, loss of jobs, but also derails in logistics, supply, or delivery. And we started craving. The moment we stepped out of it, unleashed, believing we were going back to the “old, good normal”, the global crisis and inflation hit. So, we are still torn between our wish to shop and consume, and the imposed need to prioritize and budget. But the way consumers changed their behavior depends on the category and consumers’ socio-economic level. In some categories, they started buying less or turned more to private labels. In others we observed an increase in sales of more premium brands. So, this urge to consume and spend is there, but we are reinventing and reprioritizing what is most important to us.

What is the one thing you are most proud of?

Saša: It takes a lot less time for me to reach the aha(!) moment because I believe that over time, I have improved the way I think about and approach problem-solving, and I am hopeful that this will continue.

Tara: Well, I am proud of the confidence that I have gained since I started working. When I give recommendations, I am very confident about them, and my clients act according to them. Somehow, they gave me their trust from the start; their instant confidence in me became a reason for me not to doubt myself and really feel encouraged. From that moment on, it just grew stronger.

Milica: I take pride in my diverse journey within research, spanning roles from shopper research consulting to creating and validating innovative technologies, all the way to advocating for consumer understanding through new business development.

Bratislav: For me, a business challenge has always been a creative challenge, too. So, together with clients I typically managed to design the most unusual and innovative approaches to a research problem. Very often you could consider such studies almost as pilot projects, without clear indications on how the study would end up and what the outcome would be. Fortunately, at least so far, such endeavors have ended successfully to my and the clients’ joy, which has convinced me that the “can do” attitude always pays off in the end, with a little courage, no matter how complex the challenge is, which I am especially proud of.

You look at ad and shopper behavior all the time! Ok, let’s be honest. But what kind of consumer are you?

Saša: Well, some habits never die. I used to go shopping with a list in one hand and a calculator in the other since I was a student and every penny counted, and I still do that. So, unless there is a good offer, I do not make irrational decisions impulsively. And, of course, I do the math before deciding that the discount is too good to pass up.

Tara: I am the total opposite. I want to try everything that is new. I like to try new versions of phones; I want to test every pack claim and try new flavors. When you imagine a shopper willing to engage with a product, you imagine me.

Milica: I’m sugar-free hooked! Besides that, ever since 2016, I’ve been happily immersed in the world of physical retail: whenever I hit the road, I transform into a retail explorer, tracking down mind-boggling stores across the world. To me, stores are the ultimate decision arenas. They hold the power to sway me toward novelties or classics.

Bratislav: When comparing myself to what I typically see in research studies I could say that I am quite an atypical consumer. I have my predefined set of favorite brands and usually I know what I am going to buy in advance, though I like to explore and try new things when they hit the market and quite often buy things on impulse. I rarely think about whether I am going to spend an extra buck on things I like. Typically, I assess the quality, value, and proposition a product offers rather than the costs it comes at. To illustrate my irreconcilable nature as a shopper and consumers, what may come as a surprise to many marketing people who try to “understand” consumers, if I cannot find my favorite soda (highly processed, artificially flavored) from a major brand in the store, I might as well reach for the most organic, 100% natural juice made by local small businesses.

Want to learn more about behavioral research from our experts? Find the list of EyeSee’s webinars here.

Brand blocking has long been a go-to merchandising technique for brand managers looking to ensure their brand stands out on the shelves. Although it may not seem obvious, there are several challenging questions that need to be addressed when applying this technique:

Is the brand’s portfolio broad enough so it would pay off, but not too broad to induce a paradox of choice?

What is a wider shelf/category context: price thresholds, competitors, anchor points?

Will brand blocking of certain brands support or disable category growth?

All these dilemmas arise from the fact that brand blocking is impactful on two different levels, brand growth, and category growth, and the key to success is to reconcile and align those two. To understand how to do that, we should first look at shoppers, brand managers, and category managers’ points of view separately.

Brand blocking impact on consumers

According to the Food Marketing Institute, a traditional supermarket has from 15.000 to 60.000 SKUs, or around 40.000 on average. This means that there are an enormously large number of stimuli “attacking” consumers from the shelf, so for their “defense”, they use all sorts of anchors not to feel lost. Sometimes that is a price, emotion, or a clearly communicated claim.

Simply put, in the overwhelmingly large and diverse rows of SKUs, things can get complicated, which nobody wants. Complexity leads to indecision, which could lead to walking away from categories and products.

That is why blocking should help consumers scan through shelves, allowing natural browsing patterns like book reading. It is believed that horizontal blocking makes them spend more time browsing, noticing new SKUs and smaller brands, while vertical blocking ensures loyalty and decreases switching behavior.

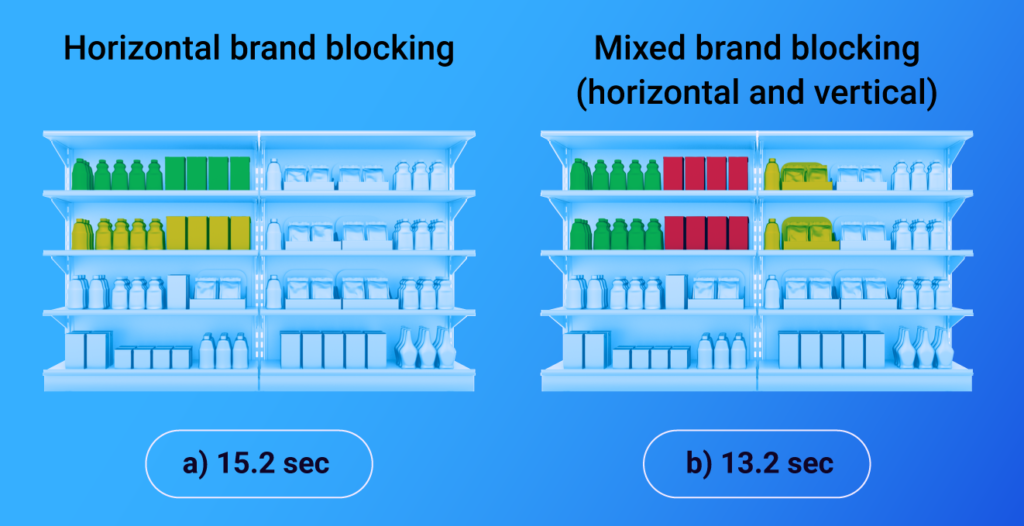

However, in a recent EyeSee study, it was proven that horizontal brand blocking of one brand, which at the same time utilizes vertical brand blocking of its subcategories, can result in a visible increase in sales.

With the speed of the “shelf scanning” cut for 2 seconds, that methodology provided 32% of sales growth. However, while this type of blocking prevents price comparisons with potentially cheaper competitors, if not placed wisely, it could experience potential cannibalization. And this leads us to a question of the brand manager’s point of view.

Is brand blocking really a must for all brands?

Brand blocking for brands looks like a no-brainer: the product is clearly visible from afar, it takes up more space, and more importantly, it covers a larger surface in the consumer’s field of view.

The whole brand portfolio should come from the same key visual that allows brand creativity to emerge. Aside from the lead color scheme, they use visual connectors, some kind of characteristic design detail that connects the group of products: a logo, a circle with the claim, a line, or even the illustration of a cat on the box of milk, whose figure is complete when we look at the product facings.

Heineken has its famous red star, and Coca-Cola has its characteristic typography with an underlying lineage.

Pack tests in a realistic shelf setting can and should be used to determine whether the pack is outstanding enough, has a clear claim, and has a strong point of difference in comparison to competitors.

However, the impact of design is not the only thing that is relevant to shoppers. Price, or value for money, plays an important role as well. For example, if we put a large pack of products from the same brand next to or close to a smaller but premium pack and they have the same or similar prices, shoppers will compare those two segments of the same brand portfolio and will use the “cheaper” one as a threshold. In this case, brand blocking can be counterproductive unless Decision Three testing is used, which can help brand managers understand the role of every product in their portfolio and how it serves different target groups.

The category manager’s role in brand blocking

By using Decision Tree or Conjoint testing, category managers can get answers on whether it is the strength of the brand or price that will influence the shopper’s purchase, but in order to find an optimal solution, that will not be the only aspect they have to integrate into their decision making. For category managers, category growth is, understandably, their top priority, and brand blocking can both help and sometimes stand in the way of that growth.

Brand blocking helps in the case when:

brand’s strengths help consumers identify certain subcategories or segments, such as health or occasion-based ones

brand is a category leader and a strong driver of innovation and change

brand assortments, or planograms, are already made with a category growth mindset

On the other hand, they must pay attention to the following:

brand blocking by brands that do not innovate, or change can lead to status-quo and the fallout of both brand volume and category

brand blocking can decrease the time that consumers spend shopping – they make decisions before coming to the store, disabling impulsive shopping on POS, which results in a smaller number of SKUs in their basket, which has a negative impact on category growth.

brand blocking isn’t fit for brands that have too narrow brand portfolios; it simply doesn’t pay off.

Conclusion

When we examine brand blocking from three different angles: consumers, brand managers, and category managers, finding the perfect category planogram is more like solving a Rubik’s cube than painting a nice, branded color scheme on the shelves.

However, it is critical to remember that both brands and retailers want the same thing: for products to move and large-volume sales to occur. To be successful, the brands’ growth visions must align with the growth mindset of the category, and vice versa. This necessitates constantly looking at the big picture and making a series of informed decisions supported by data-driven insights provided by a series of context tests of shopper behavior in realistic environments.

The power of a product claim is undeniable: 80-95% of shoppers make their purchase decisions subconsciously in stores within seconds, and over 2/3 of them do so heavily influenced by claims specifically.

After going over why no claim is universally good in the latest podcast, our top experts explored persistent industry myths, reliable claim testing practices and generally what to keep in mind when navigating the complex shopper context. Check out the full episode for more!

What (not) to do when making a solid product claim

When assessing claims, keep in mind the deep category knowledge and try to understand what matters most for a given product. Sometimes brands look at consumers’ current behavior or what needs changing; for instance, in some categories, consumers may consciously prioritize making a healthier choice. Other times, there is a tension in consumers’ lives that the product is positioned to tackle. It is essential to recognize all the influences at the very beginning of the claim development process.

The second step is to prioritize the influences. Brands tend to be very proud of their products (as they should!), and sometimes fall into the trap of trying to communicate everything. Combined with puffery and overstating the truth, claims can have a huge negative impact on consumer purchase decisions. So, say less, achieve more!

How to mitigate risks with the right research framework

The mixed-method approach is the best way to mitigate risks when selecting your product claims. For example, at EyeSee, validation studies proved that combining Eye tracking with surveys gives 2-3 times more predictivity than surveys alone.

Yes, claims test reports can be notoriously hard to read, but our team visualizes the results by plotting the claims on Relevance or MaxDiff score and Uniqueness simultaneously. By zooming in on these two metrics, brands can get a pretty good insight into which of their claims can make their product stand out.

Is testing claims in a branded context a must?

Another frequent assumption is that respondents must be aware of the brand when the product claims are tested or else the study makes little sense. However, this is not always necessary, as researchers often purposefully conduct blind tests to get a less biased idea of whether the claim works.

Well-loved, reputable brands are known to cloud judgments of claims’ believability in the sense that it is much harder to see whether any claims are ‘objectively’ vague and insufficiently substantiated. Thus, to test claims which focus on important innovation or feature, you could consider going “unbranded” to get a clearer picture of your perceived communication.

In unbranded tests, you can still tackle how the claims align with a brand by revealing the brand and asking about the claims’ brand fit in the end survey.

Sandra Stojanovic (Brand and Communications Director at EyeSee), Tara Tesanovic (shopper expert and insights Manager at EyeSee) and Nicole Tudosie (New business development Director at EyeSee), explained how to approach developing a product claim – check put the full episode for more!

We live in a complex world where consumers face vast financial pressures; however, these pressures are felt differently across the globe. Our team at EyeSee looked into how pricing adjustment strategies affect shoppers; we’ve previously published the key findings for the US market, as well as the more detailed breakdown of four tested CPG categories. Now, let’s take a closer look at the results for the APAC region.

How does APAC cope with price increases?

EyeSee has just wrapped up its first pricing study in this region to identify how consumer behavior is shifting when exposed to different pricing adjustment scenarios. In studies like these, it is important to test various categories, not only prices. The psychology of buying household items and the mindset of buying chocolate are completely different. The frequency of purchase depends on type of product category, even in the unstable times like these.

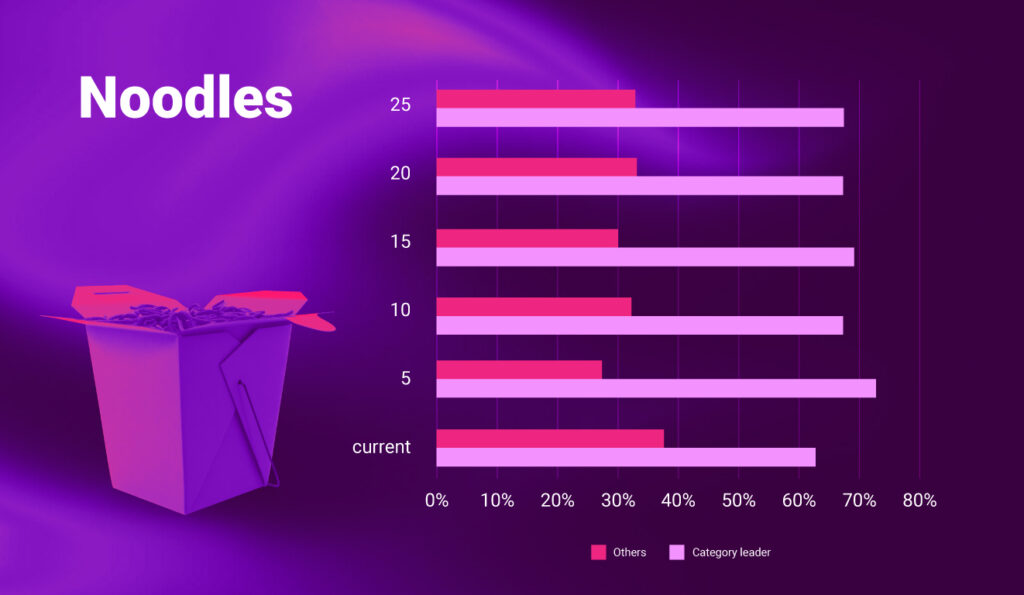

Using a conjoint exercise, we looked at four shopping categories:

2 high-frequency categories – sweets and instant noodles

2 low-frequency categories – face moisturizers and antibacterial handwash

Consumers were shown different options for increased prices – 5%, 10%, 15%, 20% and 25%.

Different adaptation scenarios are possible, and while an increase in purchasing multi-pack and big size packaging can occur for household items, it is not what would be expected for indulgence products. While certain patterns and cycles re-appear in these situations, if you are a brand, it is important to stay in touch with the consumer through research and understand in which phase of the cycle they are at, at which stage the product category is and consider all those factors to best curb the pressures of the current situation.

Here are some of the main findings.

Back to the basics and functional

Regarding low frequency categories, as the crisis prolongs, consumers are very much looking to cover the basics and stick to essentials. It is important for brands to understand that because it is what consumers search for when they are choosing among a variety of face moisturizers and antibacterial handwash. Innovation and flavors won’t be deal-breakers – it’s primarily about simplicity, price, and necessity.

When it comes to noodles, a product in the high-frequency category, the price of the category leader does not significantly impact consumer purchasing behavior. Even if the price increases, the level of purchases remains relatively stable; consumers’ attachment to the leading and well-established brand is not at risk but rather reinforced. It serves as further evidence that consumer behavior tends to gravitate towards the fundamentals/basics during uncertain times.

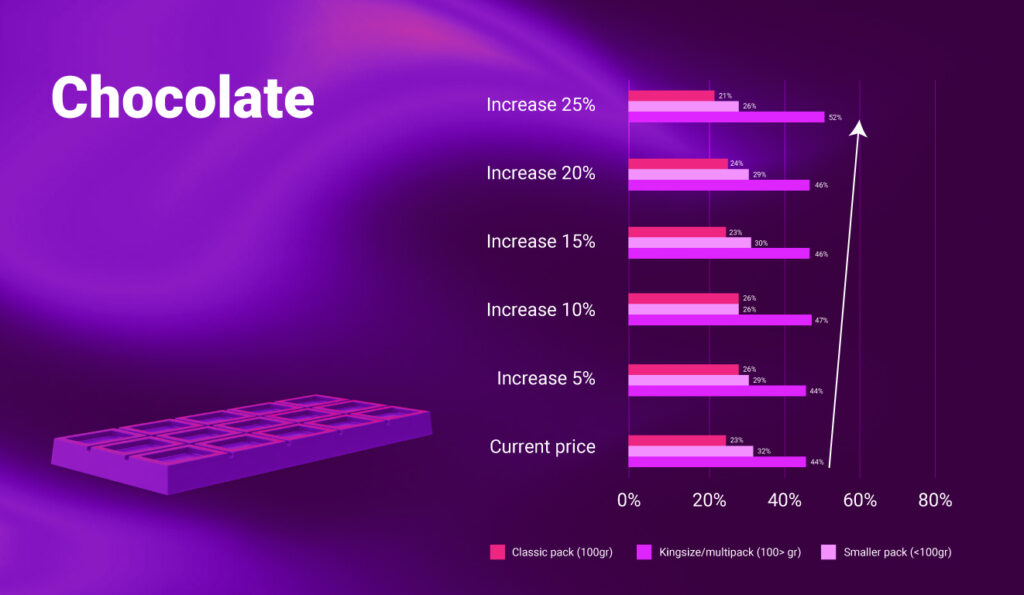

Chocolate, however, is still worth it

In our pricing study we had a category of impulse buys, such as chocolates and sweets. We observed that the inflation of prices for the small packs of chocolates doesn’t decrease their consumption. On the contrary – it has increased. At the same time, there is a decrease of consumption of the king size and multipacks with the price increase. Our hypothesis is that it is probably because small-sized chocolates are treated as a small indulgence and something extra consumers don’t want to give up on.

Knowledge and skill bring calmness and optimism

In Philippines, around 1/3 of shoppers are price-aware and savvy consumers. They are focused on price, calculate the price per unit/kilo/ounce, and know where to find products on promotions. We found that they are very optimistic with regards to their future personal financial situation, employment security and job options, financial situation in the country, as well as the global financial situation. This is probably because they have a greater sense of control over their spending, so they feel like they know how to budget and don’t feel like they have to renounce anything. Inflation, if the gap between prices and the salary is not too big, won’t ‘break their spirit’ and will keep them spending and optimistic.

(Nothing) sweet about inflation

However, for most APAC consumers, the pressure of inflation is firm, and it affects their behavior a lot. It is highly important to understand the changes in their behavior, their new needs and how it combines to influence the industry. Unpredictable times call for highly predictive insights obtained throughout relevant tools and research.

Yes, there are many price-aware consumers who can deal with all this financial pressure, but the majority still can’t handle it. They won’t reject small pleasures and treats such as small chocolate, but that is the well-known lipstick effect. In psychology, the lipstick effect describes the observation that consumers will still tend to buy small luxury items even during an economic downturn. Cash-strapped consumers want to treat themselves to something that lets them forget their financial problems and enjoy modest delight and thrill. This can’t be applied in low frequency categories like face moisturizers and antibacterial handwash because rules are different here, and consumers want only the essential and basic.

Knowing all this, it’s crucial to understand your specific categories and how consumer behavior can change swiftly depending on the needs and products on offer _____________________________________________________________________________________

Interested in findings from our pricing studies from the US and which categories have we researched? Read all about it here or you can check out the full webinar featuring Heather Graham (Director Client Service @ EyeSee), Sasa Radojevic (Sr Shopper Insight Manager @ EyeSee), and experienced retailer & Awarded 2022 Top Women in Grocery (TWiG) Raina Rusnak.

Let’s try something: google ‘sample size’ – what did you get? One of the first search suggestions that come up is definitely a ‘sample size calculator’. But let’s be honest, how applicable is it for real-life research needs?

To oversimplify, generally, the bigger the sample size, the better – more respondents, more answers, more predictive insights. But is that move always business savvy?

Let’s take a look at some cases where being smarter and creative adds value when picking the right sample size:

On your mark, get set, go psychometric

Ask any researcher, and they will tell you that the guiding light to picking the right sample size is choosing the margin of error (be it 99%, 95%, or 90% – in commercial research, 90% is typical, while in academics, 95% and 99% are the usual go-to’s). Typically, a larger sample size means a smaller error if all other variables are stable.

Following the basic psychometric principles, you would opt to have (at least) 5 times more respondents than the number of items. While traditionally, the item is a survey question, it can also be the number of SKUs on a virtual shelf. For instance, if you have 100 SKUs – the rule of thumb is to have 500 respondents.

But for shelf studies, even 300 may be enough when researching the impact on brand and category, which is most often the case. With more respondents, valid and robust insights could be made on an even more granular level of analysis.

Not every glove will fit the different methods

Of course, apart from the margin of error, the sample size also depends on the methodology used. While some surveys can include a minimum of 50-75 respondents, Virtual Shopping exercises with a standard-sized shelf need as many as 300 to collect accurate results. To further prove this, a standard (before cleaning the sample) for Facial Coding is 80, while Eye Tracking requires 60 and still yields highly predictive insights.

Why the vastly different numbers? Well, both Facial Coding and Eye Tracking provide results that are universal for humans and highly biologically determined. This means that we can use smaller samples to determine the way that people perceive specific stimuli. In other words, adding more respondents to the study will not significantly change the results, nor will it enhance the results.*

Moreover, methods such as RTM, MaxDiff, Conjoint, Findability, etc., require a certain number of people to fully complete the exercise as a minimum to get the insights we need, which can change the starting sample size.

It is also essential to keep in mind the analyses that need to be done so that the final output is robust enough at the most granular level of analysis required for the initiative. For example, as our Shopper Insights Director Dobrinka Vicentijevic explained – if you are doing segmentation and want to get 4 segments of consumers with different characteristics, you would start from the group you expect to be least represented and build the sample size from there. If the smallest group you expect to analyze is represented by around 10%, then you will need 1000 people to get 100 of them – and the same logic can be applied to other methods, starting from their minimum sample for the subgroup.

However, Milica Kovac, EyeSee’s Senior Product Manager, underlines the importance of not having too many quotas and cross-quotas in online studies – it requires real-time monitoring of each and every respondent that comes into the database and knowing exactly which quotas will close when. An alternative for some studies conducted online would be a carefully planned combination of softer quotas and statistical procedures that follow. But what should you do if you need to conduct a specific analysis (e.g., brand split) but don’t have enough users?

What Heather Graham, Client Service Director at EyeSee, believes is a solution for this is knowing the brand user volume market share. When it comes to testing pack redesigns, for example, this allows us to estimate the natural fallout of users from a category-representative sample and determine just how many are needed to boost the sample. This further ensures an analyzable base size of users for pack redesigns.

Yeah, statistics are cool, but do you know your consumer?

But then there are times when the sample size is not dictated just by the analysis – but by the end-user of the study results. For example, in category management studies (planogram and decision tree studies), the main KPI is sales potential.

So, when the client knows that 1% of real sales growth brings millions in revenue to the company, showing that 15% in sales growth is statistically irrelevant due to a small sample size is simply not the way to go. That’s why the sample is increased for the sake of usability and reliability of the obtained data for such studies.

However, if the incidence rate of a particular consumer group is extremely low – instead of increasing the sample drastically to naturally capture enough consumers from that group, an adequate sample is taken for all other required target groups instead. Then the number of people with extremely low IR is boosted as a separate sample.

Be savvy when choosing the right research design

A monadic research design entails a study in which the respondent evaluates only one product, concept or ad – rather than comparing it to different test stimuli. In doing so, you can ensure that the data you get is not influenced by any other stimuli.

But there is a good reason why sequential (monadic) designs also exist, and the insights they unlock can be priceless when compared to the standard monadic approach – especially when testing the sales potential of new products. Not only does it require a smaller sample, but by having the same people make two shopping trips, one in a competitive environment before the new product introduction and then another one with the new product launched and implemented on the shelves or webpages, it captures the all-important switching behavior and potential cannibalization effects.

Why are we talking about the design so much? Well, sample sizes are a part of the research design and having a comprehensive understanding of the design characteristics opens up room for sample size optimization!

Key takeaways:

Don’t throw psychometric principles out the window – but leave space for optimization and sample tinkering to boost the reliability of research findings

Different methods have their own rulebook –their requirements can be vastly different, so it is vital to have an in-depth understanding of each one

Know who your audience is – both in terms of who will use the data and the target audience you recruit

Be picky about research design – it is not impossible to answer more questions with a seemingly smaller sample size

*For a more detailed breakdown of choosing a sample size for these methods, check out this Proof of Method!