EyeSee has recently published the second wave of the pricing tracker in the US to look into how consumer behavior shifts when exposed to different volume and pricing adjustment scenarios.

This study had two separate exercises (virtual shopping and conjoint) and independent samples going through these exercises to obtain data for four categories.

Like last year, we tested two lower frequency categories (body wash and dishwashing) and two higher frequency categories (bacon and chips). And within these exercises, consumers faced different scenarios.

In virtual shopping, the participants looked at various scenarios, among them:

- a shelf with current pack sizes and current pricing

- increased prices on 1/3 of the shelf and the entire shelf

- decreased pack size on 1/3 of the shelf and the entire shelf.

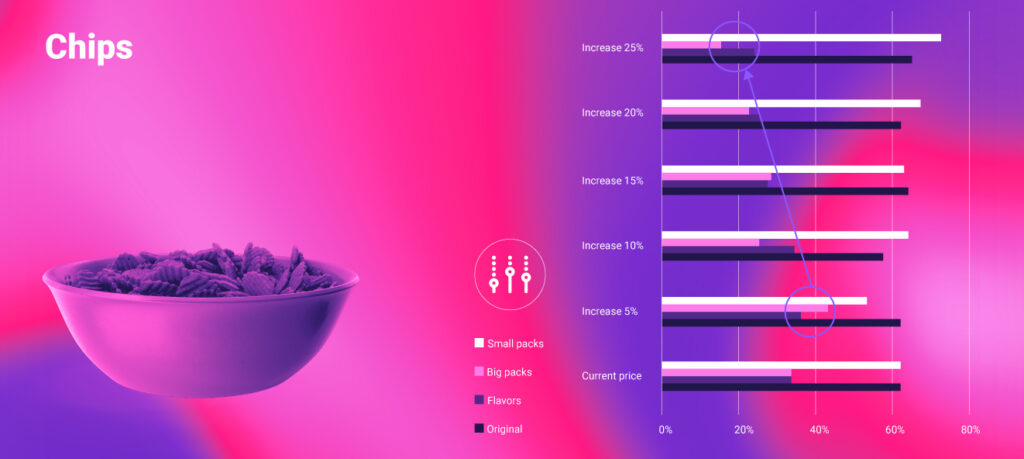

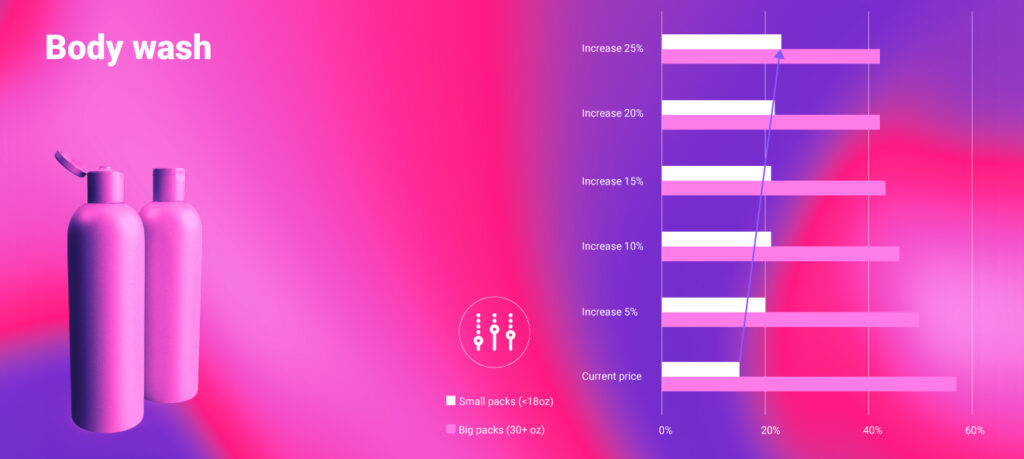

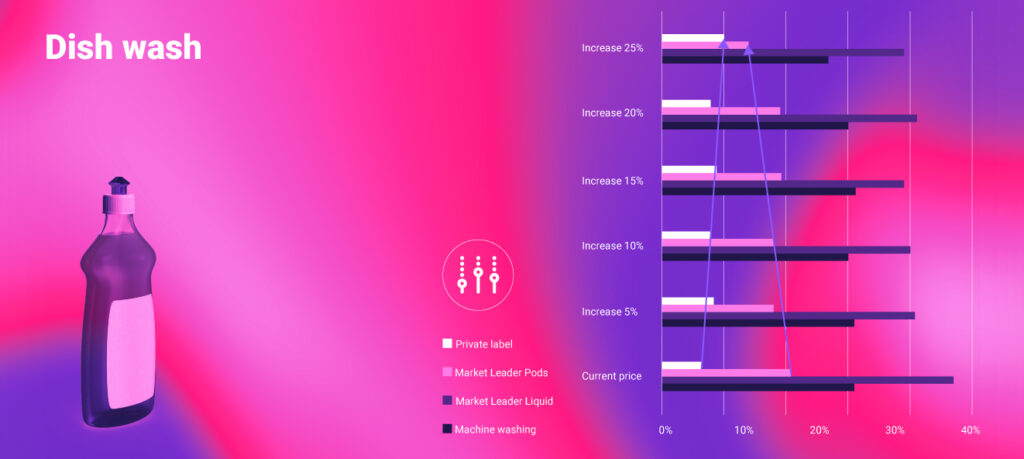

In the conjoint exercise, the respondents were faced with different price increase scenarios, as seen on the visual below – from only 5% all the way to a 25% increase, as well as a decrease in pack size.

The goal of this study was to look at two possible strategies that brands can opt for – shrinking pack sizes or increasing prices – and how do consumers react to both in the current inflation.

Let’s dive deeper into analyzed categories.

Original variants of chips and small bags remain stable

In this study, we looked at multiple chips variants such as original and flavored, but also big and small packs.

Regarding the size of a pack, a shrinking approach does matter and gets noticed – especially so for smaller volume variants. For example, if someone traditionally buys a family size pack, if the volume gets reduced by five chips, it won’t affect them and they are not going to notice that. But if we’re talking about a smaller size pack, even the smaller reduction in volume has a big impact. However, if volume stays the same, and we look at our data, on size choices, we see that people tend to forego big packs at a big price increase, and tend to replace it with a smaller bag of chips.

Also, what we noticed right away is that no matter the price increase, the original flavor pretty much remains intact. On the other hand, the same cannot be said for flavored variants that start to take a hit somewhere around a 15% price increase. We can assume that people won’t give up on chips as a basic small pleasure, but special flavors are seen as a luxury in a time when you fall back to your basics.

A reactive shift to smaller packs in the body wash category

When it comes to lower-frequency products, such as body wash, the main data cut we had a chance to investigate is between big packs with 30 oz and more, and small packs with less than 18 oz. And what we noticed is a distinct shift in buying from bigger to smaller packs – notice how white bars continue to decrease with every next price increase scenario while it is vice versa for smaller packs.

This shows us that consumers are very sensitive to the current out-of-pocket situation, trying to spend as little as they can, and they often resort to stockpiling as one of the options. As we saw in another segment of the study, people are most likely to stockpile several products such as – canned products, toilet paper, dry pasta and pasta sauces, bottled water, sugar and salt.

When does private label win in the dishwashing category?

At a macro level for dish washing products, we see that the machine-washing subcategory stays stable, similarly to hand washing products. What’s most interesting in this category is the comparison between market leaders and private label brands. The market leader liquid product, although not significant, takes a slight hit at the 5% increase and then stabilizes throughout the other price scenarios. Pods on the other hand, take a more notable hit, especially with a 25% increase scenario.

We assume that people go in part to private label pods, which nearly doubles as a choice over different increase scenarios. We know that approximately one quarter of consumers in the US are reporting that they are purchasing private label brands more often now than they were one year ago, to save money and, and to try to make their budget stretch a little bit further. This is especially true regarding products which are not personal care or indulgence. In our study, we’ve seen that the dish wash is the subcategory where we saw PL benefiting the most – so in these more practical categories, brand loyalty seems to be the least strong.

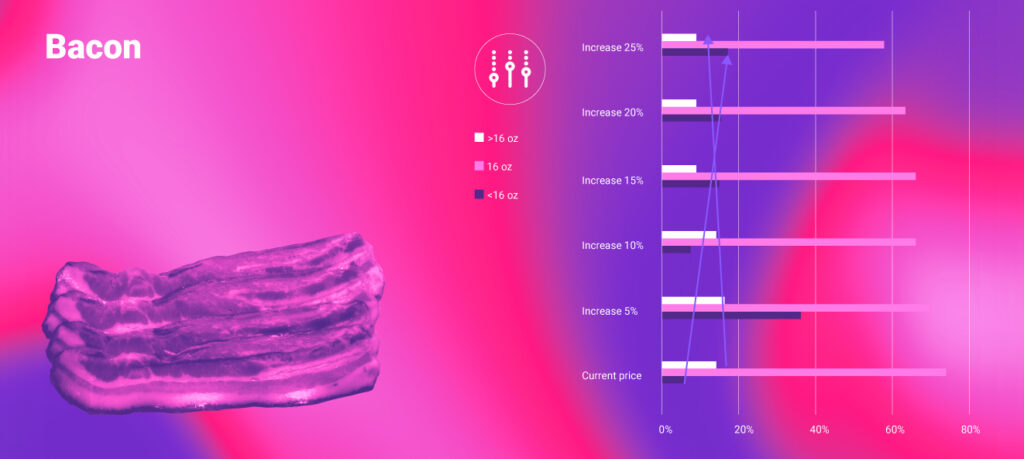

Has bacon reached a price increase threshold?

As we all know, in the US bacon plays a larger-than-life role in many consumers’ lives. It’s more than just food to them, it’s a symbol, a feeling, and an experience. So, we were intrigued to see what happened in this category.

From the conjoint exercise, we noticed that the biggest packaging options (16 oz and larger) suffer with each price increases how the big bags so suffer to a certain extent. All the while smaller packs see growth with every price increase scenario at the expense of those bigger packs.

When it comes to this category, we should also consider the historical per-pound prices. In 2021 and 2022, retail bacon prices have skyrocketed and reached the highest annual average price on record. We must keep that in mind, because those, already increased prices were used as the ‘current’ in our research. Each further price change can be a deal breaker and that’s why we can say that we have probably reached a threshold for acceptable prices of bacon for the average consumer. Customers will just walk away from the category if we increase the price too much more.

Interested in more findings from our latest study? Notice the full webinar featuring Heather Graham (Director Client Service @ EyeSee), Sasa Radojevic (Sr Shopper Insight Manager @ EyeSee), and experienced retailer & Awarded 2022 Top Women in Grocery (TWiG) Raina Rusnak.